Why autocallable ETFs are suddenly in the news

Europe has its first autocallable UCITS ETF, and the headline number is hard to miss: a coupon currently around 14% a year. That 14% figure is a current weighted-average coupon figure, not a permanent promised rate.

For investors used to plain equity trackers, bond funds and familiar iShares-style ETFs, that sounds like a very unusual income product. It is. The Calamos Autocallable Income UCITS ETF brings a structured-note strategy into an ETF wrapper. That may make the exposure easier to access, but it does not make the payoff as simple as a normal tracker fund.

Before going further, it is worth slowing down. A lot of the confusion comes from familiar words being used in a less familiar way.

Plain-English terms used in this article

- ETF means exchange-traded fund. It is a fund that trades on a stock exchange, like many familiar iShares, Vanguard or SPDR tracker funds.

- UCITS is a European fund rulebook. A UCITS fund is designed to meet EU-style rules on investor protection, diversification, liquidity and disclosure. It does not mean the investment is simple or risk-free.

- Note usually means a debt instrument. A Treasury note, or T-note, is government debt. A structured note is different: it is a debt-like investment whose payoff depends on a formula linked to something else, such as a stock index.

- Structured product means an investment where the return is built using a set formula. Instead of simply owning shares or lending money at a fixed rate, the investor receives a payoff based on conditions.

- Coupon means an income payment. In a normal bond, the coupon is the interest payment. In an autocallable, the coupon is usually conditional, meaning it is paid only if the rules are satisfied.

- Laddered means spread across different start dates, observation dates or maturity dates. A laddered strategy avoids relying on one single note issued on one single day.

The basic idea is this: the fund gives investors exposure to a laddered set of autocallable structures linked to a modified version of the US equity market. If the relevant index stays above certain levels, the strategy can pay attractive coupons. If markets fall far enough at the wrong time, the income can stop and capital losses can become much more equity-like.

This article explains what an autocallable is, why the coupon is so high, what a 40% barrier actually means, how this differs from a normal S&P 500 ETF, and why the ETF wrapper does not remove the need to understand the structured-product risk underneath.

For a deeper primer on ordinary bonds, coupons, maturity dates, principal repayment and credit risk, see AlphaSquawk’s guide to bond markets, yields and credit risk. That article explains the traditional building blocks. This article explains what happens when some of those bond-like words are used inside a more complex structured product.

The quick answer: what is an autocallable ETF?

An autocallable ETF is an exchange-traded fund that gives investors exposure to autocallable structured-note economics.

That sentence is accurate, but it can sound daunting if the terms are unfamiliar. So let’s unpack it.

An autocallable is a structured product linked to an underlying asset, often an equity index. It usually offers a conditional coupon as long as the underlying stays above a set level. It can also be redeemed automatically, or “called”, if the underlying is above another level on a future observation date.

That is where the name comes from:

- Auto: the redemption can happen automatically if the conditions are met.

- Callable: the product can be called, meaning repaid early.

More plain-English terms

- Redemption means the investment is repaid. If a note is redeemed, the investor usually receives back the amount due under the terms.

- Called means ended early. In a callable bond or autocallable note, the product can be repaid before the final maturity date if the call rules are met.

- Conditional coupon means the income payment is not guaranteed. It is paid only if the underlying index is above the required level on the relevant observation date.

- Conditional income means the same basic thing: the income depends on conditions being met.

- Underlying means the thing the payoff is linked to. In this case, the underlying is not a single company share, but an index linked to US equities.

- Observation date means a scheduled date when the product checks whether the conditions have been met.

The ETF part is the wrapper. The autocallable part is the payoff engine.

A plain S&P 500 ETF is designed to track the equity market directly. An autocallable ETF is designed to turn equity-linked risk into conditional income. This is why the wrapper matters. The product may trade like an ETF, but the return is shaped by structured-note rules: coupons, barriers, observation dates and possible early redemption.

The ETF is the box. The autocallable structure is the machinery inside the box.

That does not make the product automatically bad or dangerous. It does mean investors should not judge it as if it were a normal tracker fund.

A simple autocallable example

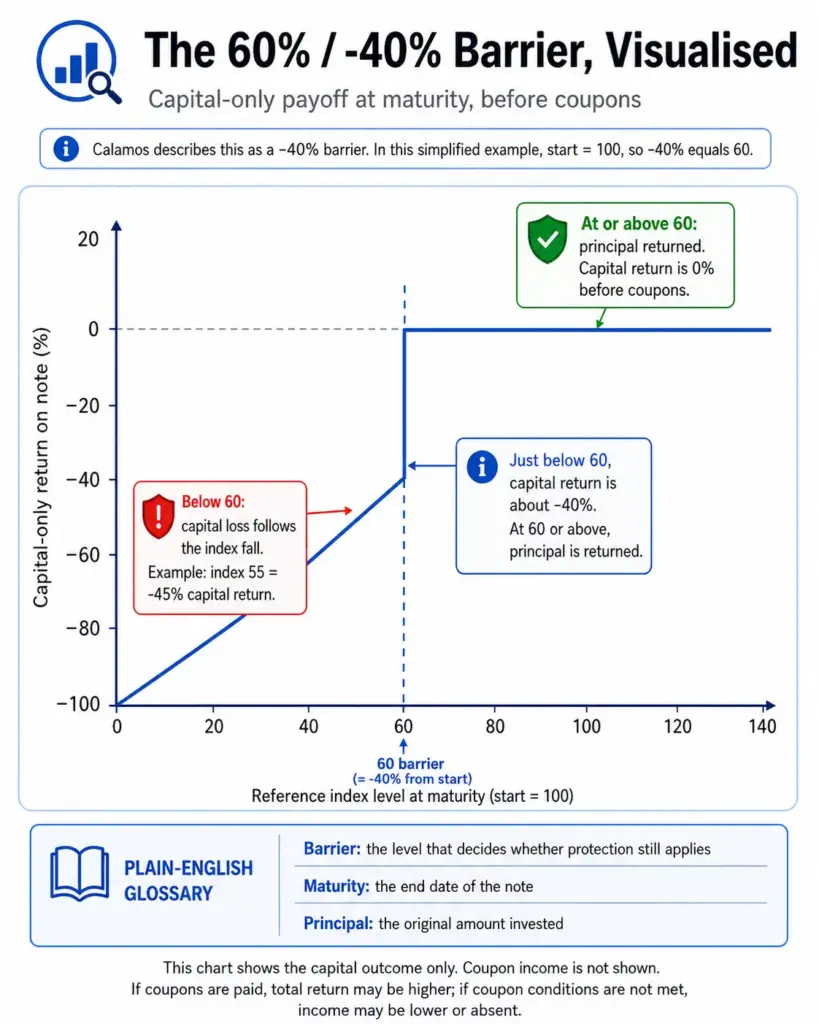

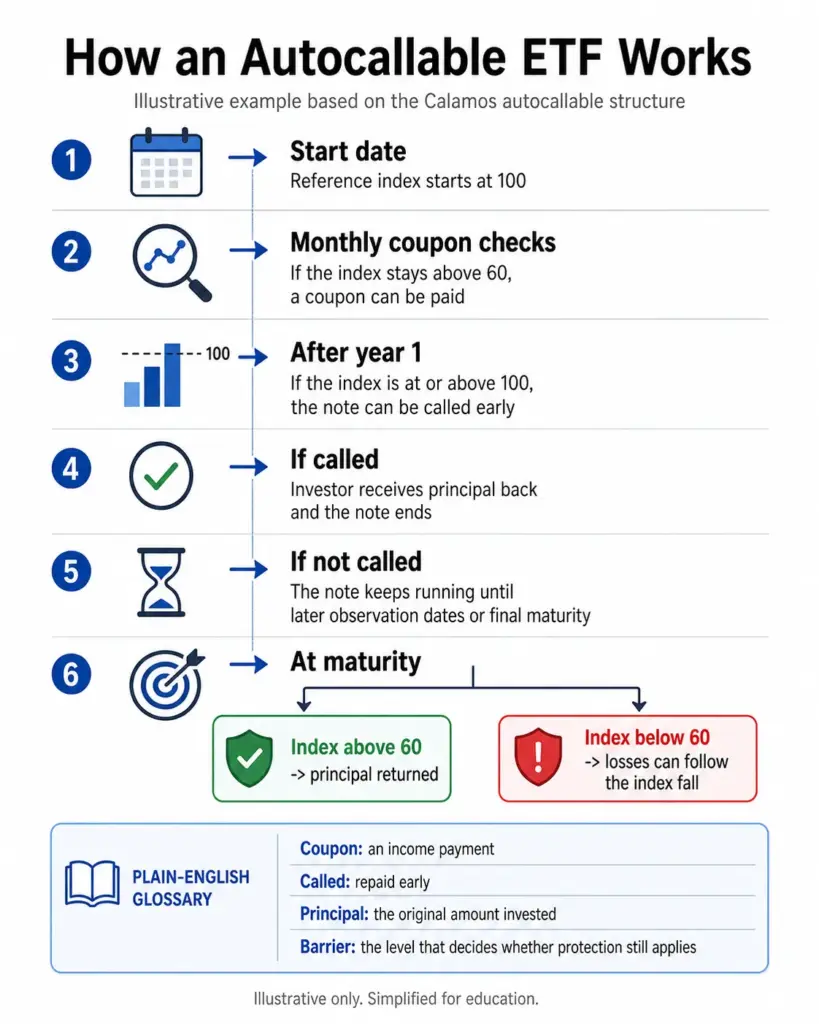

Imagine an index starts at 100.

Calamos describes both the coupon barrier and the principal maturity barrier as -40%. In plain English, that means the key barrier is 40% below the starting level. If the index starts at 100, a 40% fall takes it to 60. So throughout this article, “60% of the starting level” and “-40% from the starting level” are two ways of describing the same barrier.

A simple autocallable linked to that index might work like this:

- If the index is at or above 60 on a monthly observation date, the note pays a coupon.

- If the index is at or above 100 after the first year, the note is automatically called and the investor gets their principal back.

- If the note is not called, it keeps running until a later observation date or final maturity.

- At maturity, if the index is still at or above 60, the investor gets their principal back.

- If the index is below 60 at maturity, the investor takes a loss linked to the fall in the index.

Terms in this example

- Principal means the original amount invested, before gains or losses.

- Maturity means the final end date of the note if it has not already been called.

- Barrier means a level that decides whether protection or coupon payments still apply. A 60% barrier means the key level is 60% of where the index started. The same barrier can also be described as -40%, because the index would have fallen 40% from its starting level.

- Capital loss means a loss on the amount invested, not just a missed income payment.

So if the index starts at 100 and finishes at 55, the investor does not merely lose the 5 points below the 60 barrier. In a typical structure of this kind, the investor may be exposed to the full fall from 100 to 55. That means a 45% market fall can become a 45% capital loss.

This is why the barrier is not the same as a stop-loss. It is more like a conditional line: at or above it, the protection may still work; below it, the structure can behave much more like equity exposure.

Why the 14% coupon is not the same as a bond yield

The most important thing for a retail investor to understand is that the headline coupon is not the same as a normal bond yield.

A conventional bond usually has a stated coupon, a maturity date and a promise to repay principal, assuming the issuer does not default. That does not mean bonds are risk-free, but the basic cash-flow promise is easier to describe: coupon payments along the way, principal repayment at maturity.

Autocallables borrow some of the same language — coupon, call, maturity, principal — but the economics are different. The coupon is conditional. The repayment can happen early. The final capital outcome depends on what happens to the underlying index and whether any protection barrier is breached.

That is why a 14% autocallable coupon should not be read like a 14% bank deposit rate or a simple bond yield. The coupon is high because the investor is taking other risks: equity-market downside risk, barrier risk, reinvestment risk, derivatives risk and the risk of giving up some upside in exchange for income.

The coupon is the compensation for accepting a more complicated payoff. It is not a free lunch.

If you want to refresh yourself on how ordinary bond coupons, maturities, calls and principal repayment work, see AlphaSquawk’s guide to bond markets, yields and credit risk.

ETF, ETN, ETP and structured note: the alphabet soup explained

This story can be confusing because several similar-looking terms appear together: ETF, ETN, ETP, structured note and autocallable.

Here is the clean distinction.

| Term | Plain-English meaning | Why it matters |

|---|---|---|

| ETF | Exchange-traded fund | A fund wrapper that trades on an exchange. It may hold assets directly or use derivatives, depending on the fund. |

| ETP | Exchange-traded product | Umbrella term covering exchange-traded funds, notes, commodities and similar listed products. |

| ETN | Exchange-traded note | Usually a debt security issued by a bank or financial institution. The investor has issuer credit risk. |

| Structured note | A debt instrument whose payoff is linked to something else, such as an index, share, basket or rate. | The return depends on the formula in the note terms. |

| Autocallable | A structured product that can redeem automatically if conditions are met. | The investor must understand the coupon, call and barrier rules. |

The Calamos product is an ETF. It is not an ETN in the usual sense. But the exposure inside the strategy is linked to autocallable structured-note economics.

It is an ETF wrapper around a structured-note-style payoff.

That is different from saying it is a normal tracker ETF.

What exactly does the Calamos UCITS ETF hold or track?

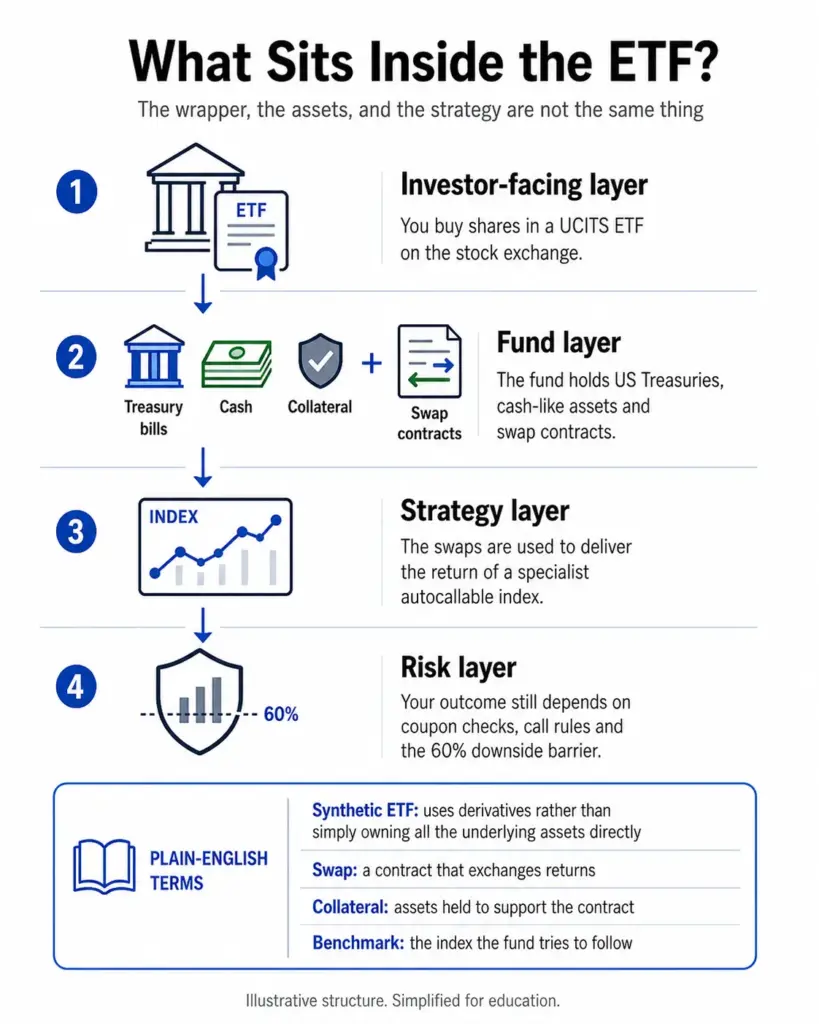

The economic story and the legal fund structure here are not the same thing.

The economic exposure is to a laddered portfolio of autocallable structures. However, investors are buying shares in a UCITS ETF, not directly buying a single private-bank autocallable note.

According to the official Calamos UCITS fund page, the fund normally invests at least 80% of its assets in US Treasuries, cash or cash equivalents, and unfunded total return swaps that provide exposure to the autocallable index. The fund page describes the product as synthetic, passive and benchmarked to the MerQube US Large Cap Vol Advantage Autocallable TR Index.

That is a dense sentence, so let us unpick it.

Terms in the fund structure

- US Treasuries are debts issued by the US government. Treasury bills, often called T-bills, are short-term versions.

- Cash equivalents are assets that behave almost like cash, such as very short-term government debt or money-market-style holdings.

- Swap means a financial contract where two parties exchange returns.

- Total return swap means a swap that passes through the total return of something, including price moves and income, according to the contract terms.

- Unfunded swap means the fund does not pay the full investment amount to the swap provider upfront. Instead, the fund keeps collateral assets and uses the swap contract to receive the agreed return.

- Collateral means assets set aside to support a financial contract and reduce the risk that one side cannot meet its obligations.

- Synthetic ETF means the ETF gets exposure using derivatives, such as swaps, rather than simply owning all the underlying assets directly.

- Passive means the fund is trying to follow a set index or rulebook, rather than having a manager freely pick investments each day.

- Benchmark means the index or reference point the fund is trying to track.

So the ETF uses a fund wrapper, Treasury bills, cash-like collateral and swap exposure to deliver the returns of an autocallable index. This is not the same as a plain physical S&P 500 ETF that simply owns the shares in the index.

The official benchmark is called the MerQube US Large Cap Vol Advantage Autocallable TR Index. That name is a mouthful, but it can be broken down:

- US Large Cap means it is linked to large-cap US equity exposure, in this case through E-mini S&P 500 futures rather than direct ownership of all the underlying shares.

- Vol Advantage refers to volatility-based rules inside the index.

- Autocallable means the index is designed around autocallable note-style payoffs.

- TR means total return.

So the simplest picture is this:

| Layer | What it means |

|---|---|

| Investor-facing layer | You buy shares in an ETF on an exchange. |

| Fund layer | The ETF holds Treasury bills, cash-like assets and swap contracts. |

| Strategy layer | The swaps aim to deliver the return of a specialist autocallable index. |

| Risk layer | The income and capital outcome still depend on coupons, barriers, market levels and contract terms. |

The fund page’s autocallable dashboard showed 59 live autocallables, a weighted-average coupon of 14.01%, and a weighted-average time to maturity of 4.5 years as of 1 May 2026. Those figures will change over time.

The modified S&P 500 exposure: not a plain S&P 500 tracker

In an FT article covering this product they describe the reference index as a modified version of the S&P 500. That is an important detail, but we need to be precise about which index we mean.

There are two related MerQube index names in this product chain:

| Layer | Index name | Plain-English role |

|---|---|---|

| ETF benchmark | MerQube US Large Cap Vol Advantage Autocallable TR Index | The specialist autocallable index the ETF is trying to track. |

| Reference index inside the autocallables | MerQube US Large-Cap Vol Advantage Index | The modified US equity index used to decide whether coupons, calls and barriers are triggered. |

So when we say “modified S&P 500 exposure”, we are mainly talking about the second layer: the MerQube US Large-Cap Vol Advantage Index.

That index is linked to E-mini S&P 500 futures, not to direct ownership of the 500 companies in the S&P 500. It also uses volatility rules. In simple terms, the index can increase exposure when markets are calmer and reduce exposure when volatility rises.

That can sound reassuring, but it introduces another layer of complexity. The investor is not just asking, “Will the S&P 500 go up or down?” They also need to understand how the volatility rules, the 6% annual decrement, the coupon checks and the 60% downside barrier combine to produce the actual result.

Terms in this section

- Reference index means the index used inside the autocallable structure to decide whether conditions have been met.

- Benchmark means the index the ETF itself is trying to follow.

- E-mini S&P 500 futures are exchange-traded contracts linked to the S&P 500. They give exposure to the index without directly owning all 500 shares.

- Volatility target means a rule designed to keep the index’s risk around a target level. Calamos says the MerQube US Large Cap Vol Advantage Index targets 35% implied volatility

- Decrement means the built-in deduction from index performance. In this case, Calamos describes a 6% annual decrement in the reference index. This is not the ETF’s annual fee, and it is not a cash charge separately deducted from an investor’s account. It is part of the index calculation and can reduce the index return used in the autocallable structure.

For a beginner, the key point is this is US-equity-linked, but it is not a plain US equity tracker. The ETF follows an autocallable index, and the autocallable index is built on a modified US large-cap equity index.

Why investors like autocallables

It would be wrong to present autocallables as automatically bad products. The appeal is real.

Investors like autocallables because they can offer high conditional income, some downside buffer before capital losses appear, and a payoff that may suit certain sideways or moderately rising markets. In a laddered ETF structure, the investor may also avoid putting all their money into one note with one start date and one maturity date.

That is the positive case. Compared with a one-off private-bank note, an ETF wrapper may improve access, transparency, operational convenience and portfolio diversification.

But none of that changes the underlying trade-off. The investor is still accepting a structured payoff. The income is conditional. The protection has limits. The upside is not the same as owning the equity market directly. And in a sharp downturn, the losses can become much more ordinary-equity-like than the coupon stream suggests.

Why the risks are easy to misunderstand

Autocallables are dangerous to explain badly because their good-case outcome is easy to understand, while the bad-case outcome is easy to underestimate.

The good-case story sounds like this: “Markets stay above the barrier, the investor receives high coupons, and the note may be called with principal returned.”

The bad-case story is more complicated: “The coupon may stop, the note may not call, the investor may remain exposed for years, and if the protection barrier is breached at maturity, losses can be linked to the full fall in the underlying from its starting level.”

The main risks are:

Coupon risk

The coupon is contingent. If the underlying index is below the coupon barrier on an observation date, the coupon may not be paid.

Barrier risk

The downside protection is conditional. If the relevant barrier is breached at maturity, the capital loss can become significant.

Early call and reinvestment risk

If the note is called early, the investor gets capital back, but that money then has to be reinvested. Future coupons may be lower if market conditions have changed.

Counterparty and derivatives risk

Because the UCITS fund uses swaps, investors also need to understand that derivatives and swap counterparties sit inside the structure.

Liquidity and premium/discount risk

An ETF trades on exchange, but that does not mean the trading price will always perfectly match the value of the underlying exposure, especially in stressed markets.

The bond-like income illusion

The biggest behavioural risk is that investors may see a steady coupon and mentally file the product beside bonds or cash. That is the wrong mental bucket. The income may look bond-like, but the risk is tied to equities, options, barriers and derivatives.

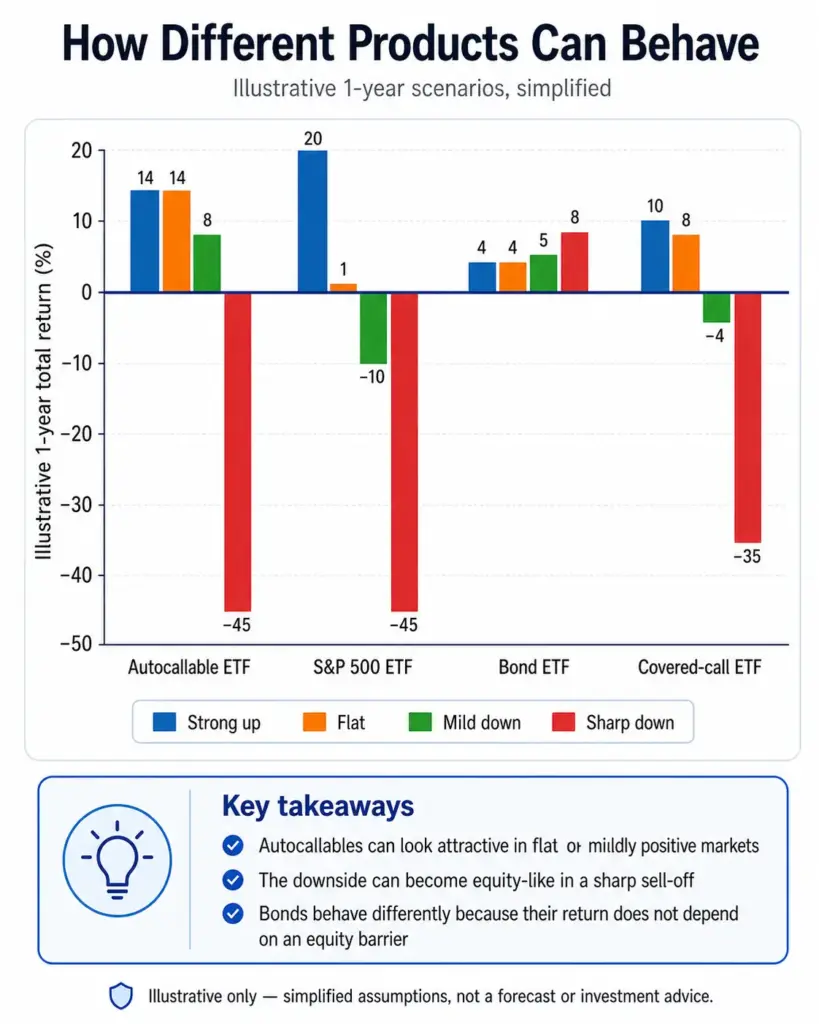

Autocallable ETF vs covered-call ETF

Some readers may already know covered-call ETFs, so it helps to compare the two.

Both strategies try to turn equity-market exposure into income. But they do it in different ways.

| Feature | Covered-call ETF | Autocallable ETF |

|---|---|---|

| Income source | Option premiums from selling calls | Structured-note coupon economics |

| Upside | Usually capped or reduced | Often limited by autocall mechanics |

| Downside | Usually still exposed to equity falls | May be buffered until a barrier, then losses can become equity-like |

| Complexity | Options strategy | Structured-note, barrier, swap and index structure |

| Main risk | Equity decline and capped upside | Barrier breach, contingent coupon and derivatives/counterparty risk |

The comparison is useful because both products can be marketed as income strategies. But an investor should not assume that “income ETF” always means the same type of risk.

Is this like private credit? The Blue Owl comparison

This is not private credit, even though both areas use debt language such as “note”, “coupon” and “income”.

That distinction matters. A reader might reasonably think: “If this is a note paying a coupon, am I basically lending money to big companies and receiving interest?”

Not really.

In a private credit fund, the fund usually lends money directly to companies outside the public bond market. The investor’s return depends heavily on whether those borrowers keep paying interest, whether the loans are valued fairly, and whether the fund can handle withdrawals when investors want their money back.

An autocallable ETF is different. The return is not mainly coming from ordinary companies borrowing money and paying interest on business loans. The return comes from a structured payoff linked to an equity index. The coupon depends on market conditions, observation dates and barriers. If the index falls too far at the wrong time, the coupon can stop and the capital outcome can worsen.

Private credit vs autocallable ETF

| Question | Private credit fund | Autocallable ETF |

|---|---|---|

| What is the basic exposure? | Loans to companies. | A structured payoff linked to an equity index. |

| Where does the income come from? | Borrowers paying interest on loans. | Coupon rules built into the autocallable structure. |

| What is the main danger? | Borrowers fail to pay, loan values fall, or too many investors ask to redeem from a fund holding illiquid loans. | The index falls below key levels, coupons are missed, barriers are breached, or derivative/counterparty risks matter. |

| Why does the wrapper matter? | A fund wrapper can make illiquid private loans look easier to exit than they really are. | An ETF wrapper can make a complex structured payoff look like a normal income ETF. |

The Blue Owl comparison is useful only at this wrapper level. Recent private-credit concerns, including redemption pressure at large retail-facing funds, show what can happen when complex income strategies are sold to a wider audience.

But the actual risks are different.

In private credit, the concern is often: “Are the loans good, are they valued properly, and can investors get out if too many people redeem?”

In an autocallable ETF, the concern is more: “Do investors understand that the coupon is conditional, the downside barrier has limits, and the product is linked to equity-market outcomes rather than a simple loan book?”

That is the useful lesson: a better wrapper can improve access, but it does not remove the need to understand what is inside the wrapper.

Questions to ask before buying an autocallable ETF

Before buying an autocallable ETF, investors should be able to answer these questions in plain English:

- Is this a plain tracker ETF, or an ETF giving exposure to structured-note economics?

- What is the underlying reference index?

- What is the coupon barrier?

- What is the capital protection barrier?

- When can the notes be automatically called?

- Is the headline coupon guaranteed, or contingent?

- What happens if the index falls 30%, 40% or 50%?

- Does the fund use swaps or direct note holdings?

- Who is the swap counterparty?

- What is the total expense ratio?

- How wide are the bid-offer spreads?

- Could the ETF trade at a premium or discount to net asset value?

- What happens in a fast crash rather than a slow bear market?

- Am I buying this for income, or am I accidentally taking equity crash risk in disguise?

If those questions feel too hard to answer, that is not a failure by the investor. It is a sign that the product needs more explanation before it deserves a place in a portfolio.

Final thoughts: accessible does not mean simple

Autocallable ETFs may be a genuine innovation. They can make a large structured-product market easier to access, potentially more transparent and cost-efficient than a one-off private-bank note

But they should not be treated like ordinary bond funds, cash substitutes or plain equity trackers.

The income is conditional. The downside protection has limits. The reference index is not a simple S&P 500 tracker. The fund uses derivatives. And if the barrier is breached at the wrong time, investors can find themselves taking equity-like losses after receiving what felt like bond-like income.

That does not make the product automatically bad. It makes it a product that needs to be understood.

The ETF wrapper is the access point. The autocallable structure is the risk engine.

Common questions and confusions

Is “premium” the same as principal?

In this context, premium usually means the amount paid into the note, while principal means the amount the investor expects to get back if the note repays at par under its terms.

For a beginner, it is safest to read both words as pointing to the same basic idea: the original capital at stake.

So if a note starts at 100 and the barrier is not breached at maturity, the simplified outcome is that the investor gets their principal back. If the barrier is breached and the reference index is down 45%, the note can suffer a 45% capital loss. The exact legal wording may use “premium”, “principal amount”, “notional amount” or similar terms, but the investor’s practical question is the same: how much of my original capital is protected, and under what conditions?

Are investors lending to companies?

Not in the same way as a private credit fund or a normal corporate bond fund.

A normal corporate bond is a loan to a company. A private credit fund usually lends money to companies outside the public bond market. The investor is mainly worried about whether those borrowers keep paying interest and repay their debts.

An autocallable is different. It uses debt-like language, but the return is mainly determined by a formula linked to a reference index. The coupon is paid only if the index is above the coupon barrier on the relevant observation date. At maturity, the capital outcome depends on whether the index is above or below the protection barrier.

So the key risk is not simply “will a company borrower repay?” The key risk is: what happens to the reference index, and what do the autocallable terms say happens at each observation date?

Do the 52-plus notes remove the risk?

No. They spread the timing risk.

Calamos’ materials describe exposure to a laddered portfolio of autocallables. The factsheet says the index portfolio is rebalanced weekly, with autocallables that have matured or auto-called replaced by new autocallables, and that the structure seeks to diversify entry points, reduce single-entry timing risk and maintain exposure to a theoretical portfolio of roughly 52 to 260 synthetic autocallables.

That matters because a single note has one start date, one set of observation dates and one maturity path. A laddered structure spreads those dates out. If there is a brief market fall and quick recovery, not every note may be affected in the same way.

But laddering does not make the product immune. A sustained market decline can affect many notes at once. Calamos itself says the reduced downside risk is relative to owning a single underlying autocallable note, not relative to investing in the S&P 500.

Is the monthly coupon really a dividend?

It may look like a dividend to investors receiving monthly income from the ETF, but economically it is not the same as ordinary company dividends from shares.

A company dividend comes from a company distributing part of its profits or cash flow. An autocallable coupon comes from the structured payoff rules. Calamos’ risk wording says coupons are contingent, not guaranteed, and will not be paid if the underlying index is below the coupon barrier on observation dates.

That is why “monthly income” is a better plain-English phrase than “dividend” when explaining the strategy mechanics.

Does the issuer only call the note when it suits them?

Autocallables are designed with automatic call rules. If the reference index reaches or exceeds the autocall level on an observation date after the non-call period, that note can be redeemed early.

For investors, the practical effect is reinvestment risk. If the note is called after favourable market conditions, the investor may have to reinvest into new notes with different coupons and terms. Calamos’ risk wording also flags early redemption risk: an automatic early redemption could force reinvestment at lower rates if market yields have declined.

The important point is not to treat the call feature as a free bonus. It is part of the bargain. The investor receives conditional income, but may give up some future upside and may have to reinvest when terms are less attractive.