Updated May 2026: This futures trading guide has been refreshed with a clearer explanation of clearing houses, margin, contract sizes, micro and nano futures, and how futures compare with CFDs and spread betting.

Introduction

Futures trading can look intimidating at first because it uses its own language: contracts, ticks, margin, expiry, delivery, clearing houses and rollovers. Underneath that jargon, the basic idea is simple. A futures contract lets traders agree a price today for an asset or financial instrument that settles at a future date.

Futures were originally built for hedging. A farmer, oil producer, airline, bank or fund manager could use them to manage future price risk. Today, the same markets are also used heavily by speculators, proprietary traders, hedge funds, algorithms and retail (non-professional) traders.

This guide explains the core mechanics of futures trading: what a futures contract is, how margin works, why clearing houses matter, what happens at expiry, and how smaller micro, mini and nano contracts have made futures more accessible to retail traders.

We will also compare futures with CFDs and spread betting, because many beginners first meet leveraged trading through OTC products before discovering that exchange-traded futures can sometimes offer cleaner pricing, centralised volume and a different counterparty structure.

Understanding Futures

The underlying market where securities or commodities can be bought and sold for immediate delivery is known as the ‘spot‘ market. In other words the underlying ‘cash’ market price right now, and this is the starting point that other tradable instruments are derived from (derivatives), with futures being one type of derivative. So first and foremost let’s begin with an introduction to futures contract components, starting with their classic definition:

A future is a legally binding CONTRACT which is an OBLIGATION to deliver / take delivery of a fixed QUALITY and QUANTITY of an underlying asset at a fixed price on a SPECIFIED DATE in the future.

It should be noted that this obligation only exists if you hold the contract to its expiry date, there is nothing to stop you passing it onto anyone else in the market that wishes to trade it from you prior to that date. It should also be noted that at expiry, many futures contracts can be cash settled for equivalent cash value, rather than involving physical delivery, but by no means all.

Some examples of futures markets include:

- Equity Index Futures e.g. S&P 500, Nasdaq 100, Russell 2000, Eurostoxx50, Dax, FTSE

- Energy Futures e.g. ICE Brent Crude Oil, Nymex Crude Oil, Natural Gas, Gasoline

- Precious Metal Futures e.g. Gold, Silver , Platinum, Palladium

- Agricultural Futures (ags) e.g. Corn, Oats, Soybeans, Wheat, Cattle, Frozen Concentrated Orange Juice, Palm Oil

- Softs e.g. Cocoa, Sugar, Coffee

- Metals Futures e.g. Iron Ore, Aluminium, Copper, Zinc

- Fixed Income e.g Government Bond futures, Interest Rate Futures

- FX Futures e.g. EUR/USD, GBP/USD, USD/JPY Futures etc.

Many exchanges offer differing size variations of their standard futures contracts which may include, ‘mini’, ‘micro’ and even ‘nano’ versions specifically to cater towards retail trader interest (and the excitement of High Frequency Trading (HFT) firms wanting to market make them). These smaller contracts match the price of their larger counterparts nearly always but have smaller tick values and smaller margin requirements which reduces risk exposure.

Futures and Forwards

Futures contracts are very similar to forward contracts being that they both represent a pledge to carry out a specific transaction at a future date. Although futures differ from forwards in that they:

- Trade on a regulated futures exchange.

- Are guaranteed by clearing houses.

- Have a margin requirement to be settled on a daily basis i.e. they are ‘marked to market’.

- Are standardised

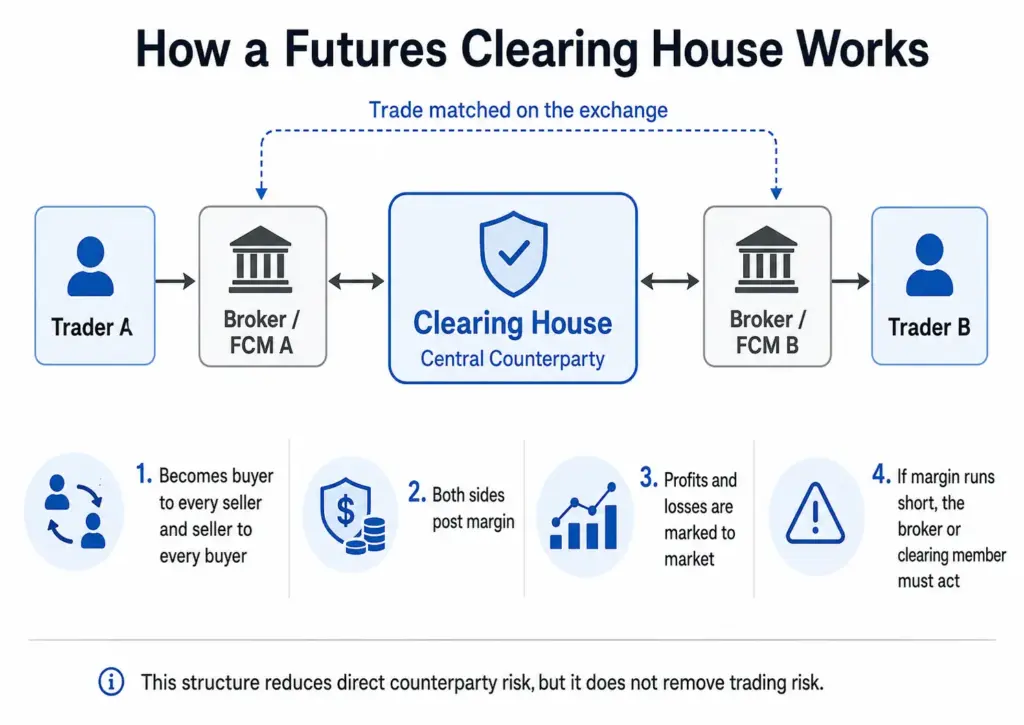

How Futures Clearing Houses Work

One of the biggest differences between futures and private forward contracts is the clearing house.

When two traders agree a futures trade on an exchange, they are not usually left facing each other directly until expiry. The clearing house steps in between them through a process known as central counterparty clearing. In simple terms, it becomes the buyer to every seller and the seller to every buyer.

That matters because your trade is not dependent on one random trader on the other side paying up. The clearing system manages risk through margin (effectively a safety deposit explained later), daily mark-to-market settlement, clearing members and default procedures.

A simplified version works like this:

- you place a trade through your broker or Futures Commission Merchant;

- the trade is matched on the exchange;

- the clearing house becomes the central counterparty;

- both sides must post margin;

- profits and losses are marked to market, usually daily or intraday;

- if a trader cannot meet margin requirements, the broker or clearing member must deal with the problem before losses build up.

This does not mean futures trading is risk-free. You can still lose money very quickly, and broker or FCM failures can create administrative and legal headaches. But the clearing-house structure is one reason regulated futures markets are generally more transparent than private OTC (over-the-counter) products such as CFDs, spread bets and forwards.

Standardisation of Futures

The standardisation of futures contracts involves various elements:

- What the underlying asset or instrument is (such as barrels of oil or interest rates).

- Whether the settlement of the contract results in actual physical delivery of a product or cash settlement to the same value.

- The amount and units of the underlying asset per contract.

- The currency in which the futures contract is quoted.

- The grade of the deliverable. eg NYMEX Light Sweet Crude Oil contract specifies sulphur content and API specific gravity, as well as the pricing point – the location where delivery must be made.

- The delivery month and last trading date.

- Other details such as the tick value – the minimum permissible price fluctuation.

A generic commodity futures contract will therefore have its:

- Units of trading, such as bushels (wheat), barrels (oil), the quantity of them per contract and any composition (quality) requirement.

- Delivery months e.g. March, June, Sep, Dec if looking at something like T-notes or equity indices with good quarterly volume expiries.

- Standard of delivery – cash or physical and required delivery location.

- Quotation per unit e.g. dollars and cents for oil.

- Minimum price movement e.g. for CL Nymex oil – $10 per tick (1 cent x 1000) where the CL contract represents 1000 barrels of oil per contract. So if you buy a 1 lot at $85.30 and sell it at $85.31 would would have made $10 before deducting the cost of the trade.

Grasping the Terminology

Any introduction to futures trading wouldn’t be complete without highlighting some of the terms and concepts:

- Leverage: Futures trading enables you to control a substantial amount of the underlying asset with a relatively small amount of capital, known as leverage, which can amplify both gains and losses.

- Margin requirements: Because of this leverage, to trade futures you must have enough money to open a position (initial margin) and maintain a certain amount of capital in your account thereafter, called the maintenance margin. If your account balance falls below the maintenance margin, you will receive a margin call and be required to deposit additional funds or have your position closed out.

Margin rates are listed on exchange websites such as CME (Chicago Mercantile Exchange), Eurex and ICE (Inter-continental exchange) and they vary from time to time depending on how volatile or illiquid the markets are, the greater the risk of movement the higher the margin required. If you only trade intraday, many retail brokers will give you reduced intra-day margin requirements, although if you deal with institutional providers many have recently been demanding even greater amounts than the exchange’s initial margin requirements. - Tick value: A tick represents the minimum price movement for a futures contract, and each tick has a monetary value, known as the tick value, which varies depending on the specific contract (see the oil example in the section above). These tick values can be found under the contract specifications on the exchanges’ websites.

- Expiration date: Each futures contract has a predetermined expiration date, after which the contract ceases to exist. Traders must close i.e. trade out of, or ‘roll over‘ their positions (close out in the old expiry contract and open in the new expiry contract) before this date to avoid requirements around physical delivery or cash settlement. Most retail brokers will not let you trade or hold positions in contracts which are close to expiry as dealing with expired futures positions can be extremely costly, particularly in contracts which involve physical delivery.

- Limit Moves Some futures contracts have exchange-set price limits that restrict how far the contract can move during a trading session. If the market hits the limit, it may trade only at that limit price, pause, reopen with expanded limits, or remain effectively locked depending on the product and exchange rules. This matters because you may not be able to exit normally. I have seen this personally, even in equity index futures during the 2008 financial crisis, when rescue-package announcements and coordinated central-bank action produced violent repricing. ES (e-mini S&P futures) traders may go years without seeing a serious locked market, but when it happens it is not theoretical. A day trader using reduced intraday margin can suddenly be facing full overnight margin, or may need to hedge on another exchange without getting the margin offset they expected. Agricultural futures have historically been more prone to repeated limit-up or limit-down sessions, where the market opens locked for several sessions and there is not much a trader can do except manage the risk around it.

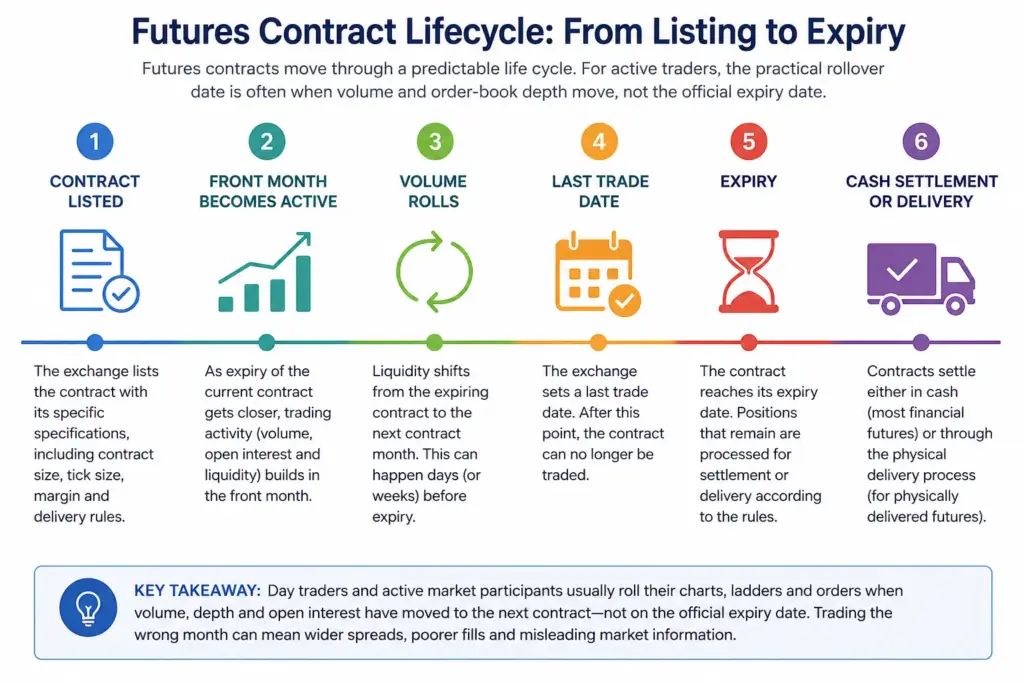

Contract Months, Front Month and Rollover

Futures contracts trade in specific expiry months. Some products have monthly expiries, while others trade most actively in quarterly months such as March, June, September and December.

On trading screens, futures months are often shown with single-letter month codes. For example, March is H, June is M, September is U and December is Z. So a June E-mini S&P 500 contract may appear as something like ESM followed by the year, depending on the platform. CME lists the standard month code system used across futures markets.

The most active nearby contract is often called the front month. Some traders also use the phrase prompt month, especially in commodity markets, to refer to the nearest deliverable or most immediate trading month. This is usually where the best liquidity sits, but that can change as expiry approaches.

Rollover is the process of moving from one contract month to the next. If you are long the expiring contract, rolling normally means selling that contract and buying the next active month. If you are short, it means buying back the expiring contract and selling the next active month.

For day traders, the important point is that you do not normally wait until the expiry date to change your charts and ladders. You roll when the volume, order-book depth and open interest have clearly moved into the next contract. In practice, this can happen days before expiry, and the timing varies by product.

That matters because trading the wrong month can give you poor fills, wider spreads and a misleading read of order flow. If everyone else has moved from the March contract to the June contract, but your chart and DOM are still focused on March, you may be watching yesterday’s market.

Rollover is also why continuous futures charts need care. A continuous chart stitches together different contract months, but the real traded contracts still expire. For backtesting, technical analysis or spread analysis, you need to know whether your chart is using the front month, a back-adjusted continuous contract, or a specific expiry.

Mini, Micro and Nano Futures Contracts

One reason futures have become more relevant to retail traders is the growth of smaller contract sizes.

Traditional futures contracts can be large. A single standard futures contract may represent a meaningful amount of oil, gold, wheat, equity index exposure or interest-rate exposure. That was fine when the main users were producers, banks, funds, brokers and professional trading firms, but it was often too large for smaller individual traders.

Exchanges have responded by offering smaller versions of popular contracts. Depending on the market, you may see full-size, mini, micro and even nano contracts.

For example, the Micro E-mini S&P 500 futures contract gives exposure to the S&P 500 at a much smaller multiplier than the larger E-mini contract. That means a trader can scale position size more carefully and needs less capital per contract.

This has helped futures compete more directly with CFDs and spread betting for retail traders. A retail trader who previously used a CFD provider for smaller index exposure may now be able to trade a smaller exchange-traded futures contract instead.

That does not automatically make micro futures cheap. Commission, exchange fees and data fees still matter, and the cost per tick can be high relative to the profit target if you are scalping tiny moves. Smaller contracts reduce exposure, but they do not remove leverage or trading risk.

Participants in Futures Markets

There are two main types of participants in futures markets: hedgers and speculators. Hedgers use futures contracts to protect against adverse price movements in the underlying assets, while speculators aim to profit from these price movements. Both types of participants play a crucial role in providing liquidity and facilitating price discovery in the futures markets.

As futures trading is a zero sum game i.e if you make money someone has to lose the same amount on the other side, you need to understand who you are trading against and what they are doing in the market. A large bond fund may unwind a massive position over a few days moving the market significantly, yet an intraday mean reversion spread trader will have a completely different short term agenda. Only if you get into the mindset of what are known asother timeframe participants compared to you, can you learn to be fluid around their actions and profit from them. Arbitrage algorithm firms such as Citadel or Jump might be interested in having a position for only milliseconds or less.

Trading Futures Spreads

Not all futures trading is a simple outright (flat price) bet on whether a market goes up or down.

Many professional futures traders also trade spreads. A spread trade involves buying one futures contract and selling another related futures contract at the same time. The trader is then trading the price difference between the two legs, rather than only the flat price of one contract.

Common examples include:

- Calendar spreads: buying one expiry month and selling another expiry month in the same market, such as buying June crude oil and selling July crude oil.

- Inter-commodity spreads: trading the relationship between related markets, such as crude oil versus refined products, or one grain against another.

- Inter-market spreads: trading related contracts listed on different exchanges or linked to different benchmarks.

- Butterflies: a three-legged spread that combines two calendar spreads. For example, a trader might buy one nearby month, sell two of the middle month, and buy one later month.

Spread trading is often less about “will this market go up?” and more about “will this relationship widen, narrow, steepen or flatten?” That can make it useful for traders who understand the underlying market structure.

It does not remove risk. Spreads can move sharply, especially around expiry, delivery squeezes, inventory shocks, weather events, central-bank meetings or changes in market positioning. But for many futures traders, spread trading is a major part of the market and not an advanced afterthought.

Settlement and Delivery

Futures contracts can settle in two main ways: cash settlement or physical delivery.

Cash-settled futures do not involve anyone delivering the underlying asset. Instead, the contract is settled financially against a reference price or index. Many equity index futures are cash settled, which is one reason they are easier for financial traders to understand.

Physically delivered futures are different. If the contract is held into the delivery process, the buyer may have an obligation to take delivery of the underlying asset, while the seller may have an obligation to deliver it. The exact delivery rules depend on the contract specification: grade, quantity, location, timing and delivery procedure all matter.

This does not mean a normal retail trader is likely to wake up with crude oil, wheat or cattle on the doorstep. A competent broker or FCM should prevent a retail account from holding a physically delivered contract too close to expiry if the client is not approved and operationally able to handle delivery. Many brokers force liquidation, block new trades, or impose earlier internal deadlines well before the exchange’s final delivery process begins.

Even so, the delivery mechanism still matters because it can affect the price of expiring futures in extreme situations.

The famous example is WTI crude oil in April 2020. The May 2020 WTI futures contract collapsed into negative territory just before expiry, settling at around negative $37 per barrel. This was not because people thought oil had no long-term value. It was a delivery, storage and positioning problem.

The expiring contract was tied to physical delivery at Cushing, Oklahoma, at a time when storage was under severe pressure. Traders and speculative product managers that could not take delivery needed to exit or roll their exposure, while there were not enough willing buyers with storage capacity to absorb the selling. Futures-based oil ETFs and other financial longs were part of the wider pressure, but it is too simple to say one ETF alone caused the negative price.

The nearby futures contract became a problem of storage, delivery, expiry mechanics and forced position management, not just a simple oil-price view.

That episode is a useful warning for beginners. The expiry month matters. The delivery terms matter. The contract you are trading matters. A cash-settled equity index future and a physically delivered crude oil future do not carry the same operational risk.

If you are long a futures contract and hold it into delivery, you are the side that may have to take delivery of the underlying asset. If you are short and hold into delivery, you may be the side expected to provide it. In physically delivered markets, that is a real contractual obligation, which is why most retail traders close or roll positions well before that stage.

Note: Cheapest to Deliver in Bond Futures

In some physically delivered futures, especially government bond futures, the seller may have a choice of which eligible bond to deliver. The cheapest to deliver (CTD) is the bond that is most economical for the short side to deliver after allowing for the contract’s conversion factors and delivery rules.

For beginners, the key point is simple: a bond future is not always “one bond”. It may represent a basket of eligible bonds, and the market price can be influenced by which bond is expected to be cheapest to deliver.

Physical Hedging Example

As a simplified example imagine you are a coffee farmer in South America and bad frost is forecast at a critical time in your crop’s development. The price of coffee futures for the expiry around harvest time, several months away, spikes higher as speculators see the weather maps and take on long positions to profit on their prediction. They assume with more frost damage to the crop there will be less of it around come harvest time, so with no forecast drop in demand for coffee but a reduced supply, economics tells us prices will increase. Starbucks and Costa customers still want their coffee.

The frost comes and goes, you as the coffee farmer found your crop barely affected by the frost, the same as your neighbouring farmer friends, in fact you think you are still on track for a bumper harvest. So your opinion is that the price spike will be short lived and prices will come down hard. You can’t sell your coffee yet, as it’s not ready but you can open a short futures position for a number of contracts close to the amount of the coffee you will harvest. You might look up the C Coffee futures contract specs on ICE and see it’s 37,500lbs per contract, so you sell an offsetting amount compared to your production as a hedge. This has the effect of locking in this spike high sale price for your coffee – happy days. This leads to several scenarios.

- If the price continues higher, as the rest of the South American harvest was decimated by the frost and you just had a warm valley, you could sell your harvest for even more money but you will have lost money on your short futures position. So net-net you locked in the price you sold at overall.

- If the price drops as you predict, because there’s little frost damage and lots of farmers sell a bumper crop at harvest time as you predicted, you will end up selling your harvest for less money than the spike price but you will have made money on your short futures position to compensate, so once again you locked in the high sale price effectively.

You could either deliver the coffee against the short futures contract by holding it to expiry or you could close out your futures hedge prior to expiry.

Many producers and significant purchasers hedge some of their exposure to price fluctuations in this manner, as it can provide some balance sheet stability and make planning easier for accountants as to what costs and revenues will be. However if you hedge you can lose out on preferable market moves in your favour and nobody has a crystal ball. A firm like Emirates Airlines does not hedge its aviation fuel purchases, it is fully exposed. This is a management decision, traders and forecasters are often wrong and in house traders or external hedging brokers bring their own costs and issues but the choice is there to be made.

Selecting a Broker

Choosing a trustworthy and reputable futures broker or Futures Commission Merchant (FCM) is essential for a successful trading experience. The broker should provide access to the necessary trading platforms, charting tools, and order types for your preferred trading strategies. Additionally, consider factors such as transaction costs, intraday margin requirements, and customer support when comparing them and do some research on their financial viability. Anyone who had money tied up during the MF Global collapse knows that even regulated market structures do not make broker failure painless.

When comparing brokers, do not look only at the headline commission. Futures brokers usually show explicit costs such as commission, exchange fees, clearing fees and data fees. CFD and spread betting providers may advertise zero commission, but the cost may be hidden inside a wider spread or overnight financing charge. For active traders, the wider spread can easily matter more than the visible commission.

Developing a Trading Plan

Creating a robust trading plan is a crucial component of futures trading success and being successful at trading any other product. Your trading plan should outline your trading goals, risk management guidelines, and specific trading strategies. It should also include a comprehensive understanding of the market structure, technical analysis, and key factors that influence price movements.

- Risk management: Effective risk management is vital to protect your trading capital, in addition to setting stop-loss parameters it should also consider appropriate leverage, times when you should or shouldn’t be in the market and psychology – both yours and the market’s. Even if you plan to automate you trading, fear and greed still drive markets and so psychology should always be a consideration when coding an algorithm. Some of the most panicked moves in the market are actually driven by fearful, badly coded algorithms which feed off each others’ actions like spooked cats.

- Technical analysis: Technical analysis involves using charting tools, specifically indicators, to analyze historical price data to help predict future price movements but the term is bundled in with general charting which tends to focus more on patterns and volume. Common chart types used in futures trading include candlestick charts, volume profile charts, and market profile charts.

Market Profile (TPO-Time Price Opportunity) and Volume Profile are advanced charting techniques that display price and volume data in a unique format, helping traders visualize the market’s auction process, identify value areas, and locate the point of control (POC) – the price level with the highest trading activity. - Fundamental Analysis: Critical in knowing what is driving your market and protecting your account from surprise moves. We have a whole article on fundamental vs technical analysis that goes deep into strategy which I strongly recommend.

- Order flow: Order flow refers to the real-time flow of buy and sell orders in the market. By analyzing order flow data, such as the Depth of Market (DOM), traders can gain insights into the market’s liquidity, supply and demand, and potential short term price movements.

- Trading strategies: Various trading strategies are available to futures traders, including directional strategies such as momentum trading which focus on outright or flat price trades, spread trading where one position offsets another or mean reversion trades, and scalping also known as jobbing, which is high frequency trading for small profits involving analyzing order flow.

It is essential to choose a strategy that aligns with your risk tolerance, trading style, and market knowledge. The book, Enhancing Trader Performance by Brett Steenberger, gives extensive guidance on how to find your niche trading style.

Trading Sessions and Market Hours

Futures markets operate in different trading sessions, including overnight sessions and regular trading hours (which used to be pit sessions) although the trend is towards near 24hr trade, 5 days a week. It is crucial to be aware of the trading hours for your specific futures contracts, as market conditions and liquidity can vary significantly between sessions as well as the margin requirements demanded by your broker at different times. Additionally, understanding the concepts of balance and imbalance in the different sessions can help you identify potential trading opportunities based on auction theory.

Limit moves are another reason futures traders need to understand the session they are trading. A position that looks manageable during normal liquidity can become a very different problem if the market locks at its limit, liquidity disappears, and the broker’s intraday margin concession no longer applies.

Advantages of Futures Trading

Futures trading offers several advantages to traders and investors, including:

- Leverage: The ability to control a large amount of the underlying asset with a small amount of capital, potentially amplifying returns.

- The same price seen around the world: Unlike something like CFDs or other over the counter (OTC) products like cash forex, everyone trades on centralised regulated exchanges (ignoring non-regulated futures venues like the defunct FTX) and everyone knows exactly how many contracts traded at each price with the same high and low prices. CFD and FX providers rarely have the same high and low prices as their competitors particularly in times of panic such as the Swiss currency de-pegging where they were hundred of prices different to each other and several firms went bust.

- Reduced counterparty risk: unlike CFDs, forex or spread bets, regulated futures are centrally cleared. The clearing house steps between buyers and sellers and manages performance through margin and mark-to-market settlement. That does not remove every possible risk, but it is a very different structure from trading directly against an OTC provider.

- Diversification: Access to a wide range of asset classes, including equities, commodities, and currencies, and short selling in them is as easy as going long (buying) allowing for portfolio diversification and hedging.

- Short selling: The ability to profit from falling market prices by selling futures contracts short without calling a broker to borrow stock on your behalf, as is required when shorting individual stocks.

- Tax benefits: Futures trading may offer favorable tax treatment compared to other investment vehicles, depending on your jurisdiction.

- Lower transaction costs: Futures trading often involves low visible execution costs in liquid markets. Although futures brokers charge commissions and exchange fees, the tight exchange spread can still make them cheaper than some “commission-free” CFD or spread betting products, where the real cost is hidden in a wider bid/ask spread.

Starting with Futures Trading

- Learn the market: Educate yourself on the specific futures contracts you wish to trade, including their contract specifications, tick values, and margin requirements.

- Develop a trading plan: Create a comprehensive trading plan that outlines your trading goals, risk management guidelines, and trading strategies.

- Get yourself set up with a futures trading journal, it needn’t be anything fancy, just a notebook or excel sheet will do but there are fancier alternatives.

- Practice with a demo account: Before risking real capital, practice trading with a demo account to build your skills and test your trading plan.

- Open a brokerage account: Choose a reputable futures broker or FCM and open a brokerage account that meets your trading needs and capital requirements, only put in what you can afford to lose.

- Start trading: Once you’ve given yourself an introduction to futures trading on a simulated account, feel confident in your trading abilities and have a solid understanding of futures trading concepts, you can begin trading with real money. Start very small and grow your confidence in your strategy before incrementally increasing the number of contracts you trade over time.

I began on a 1 lot clip (EUR12.50 per tick) in 2002 trading Euribor futures (3 month interest rates) after 3 months on the sim and within 5 years I was clipping 400 lots in the bund (10yr German Bond) as an intraday trader doing 20-30 trades a day, although the bid ask size used to be a few thousand lots at each price back then, whereas today it’s only a few hundred. With the introduction of micro and nano futures, you can start much smaller although I would recommend getting off these as soon as possible if actively day trading as they work out to be expensive in terms of costs relative to what you make per tick. Also make sure you are trading the active contract month. For day trading, I would generally rather follow the contract where the volume and DOM depth have moved than cling to the old month just because it has not technically expired yet.

Futures vs CFDs and Spread Betting

Many beginners arrive at futures after first seeing CFDs or spread betting platforms. The products can look similar on the screen because all three allow traders to speculate on market direction with leverage.

The structure is different.

Futures trade on regulated exchanges with central clearing, standardised contract specifications and visible exchange volume. CFDs and spread bets are usually over-the-counter products where the provider creates the price around an underlying market and acts as your direct counterparty.

The cost structure is also different, and this is where many beginners get misled.

A CFD or spread bet platform may advertise “zero commission”, but that does not mean the trade is free. The cost is often built into the bid/ask spread, overnight financing, expiry adjustment, or the provider’s pricing around the underlying market.

Futures usually look more expensive at first because the costs are visible: exchange fees, clearing fees, regulatory fees and broker commission. But visible does not always mean higher.

For example, take a Bund-style market where one futures contract is worth €10 per tick. If a CFD provider quotes a six-tick-wide spread and you trade the equivalent of €10 per tick, the spread alone represents about €60 of execution cost if you buy and immediately sell. By contrast, if the exchange-traded futures market is trading at a tight spread (usually zero) and you are paying only explicit commissions and exchange fees, the real execution cost may be far lower, typically less than €2.

That is why “commission-free” can be a trap. The better question is not whether a platform charges commission. The better question is:

– how wide is the spread?

– is the price based directly on the exchange-traded market?

– are there overnight financing charges?

– are there expiry or rollover adjustments?

– what size are you trading?

– how much slippage do you usually suffer?

– are you trading against a central order book or an OTC provider?

That does not mean futures are always the right choice. CFDs and spread bets can offer very small trade sizes, simple platform access and, in the UK, spread betting has a distinct tax treatment. They can also be useful for markets where the futures contract is too large, too illiquid, or awkward for a small account.

But for liquid markets such as major equity indices, government bond futures, interest-rate futures, some commodities and major FX futures, exchange-traded futures can sometimes be cheaper than “commission-free” OTC products once the full spread and financing cost is included.

The rise of micro and nano futures has made that comparison more interesting. Smaller futures contracts now compete more directly with the small position sizes offered by CFD and spread betting providers.

For a deeper comparison, see our guide to CFD trading vs spread betting, where we explain the differences in pricing, tax treatment, expiry dates, overnight charges and OTC provider risk.

Conclusion

Futures trading gives individual traders access to the same exchange-traded markets used by hedgers, funds, banks, proprietary traders and algorithms. That access can be powerful, but it comes with leverage, margin calls, expiry dates and the need to understand contract specifications.

The biggest beginner mistake is treating a futures contract like a simple bet on direction. Before trading live, you need to know the tick value, margin requirement, expiry, settlement type, trading hours, liquidity and what happens if the market moves sharply against you.

Micro and nano contracts have made futures more accessible, but they have not made them harmless. Start small, understand the product, keep risk controlled, and compare the real costs carefully against CFDs, spread betting and other leveraged alternatives.

Key Takeaways

- A futures contract is a legally binding agreement to deliver or take delivery of a fixed quality and quantity of an underlying asset at a predetermined price on a future date.

- Futures contracts can be found in various markets, including equity indices, energy, precious metals, agriculture, and foreign exchange, among others.

- Futures contracts are standardized, traded on regulated exchanges, and guaranteed by clearing houses. They have daily margin requirements to settle and are marked to market.

- Two main participants in futures markets are hedgers, who use futures contracts to protect against adverse price movements, and speculators, who aim to profit from these price movements.

- Futures contracts can be settled in two ways: physical delivery or cash settlement, with most individual traders preferring cash-settled contracts.

- Selecting a trustworthy and reputable futures broker or Futures Commission Merchant (FCM) is crucial for a successful trading experience.

- A robust trading plan that outlines trading goals, risk management guidelines, and specific trading strategies is a crucial component of futures trading success.

- Futures markets operate in different trading sessions, including overnight sessions and regular trading hours, with different margin requirements and liquidity levels.

- Futures trading offers several advantages including leverage, diversification, the ability to profit from falling prices (short selling), potential tax benefits, and lower transaction costs compared to trading underlying assets directly.

- Getting started in futures trading involves educating oneself on the specific futures contracts, developing a trading plan, practicing with a demo account, opening a brokerage account, and gradually beginning to trade with real money.

- The front month or prompt month is usually the nearest active contract, but traders should watch where volume, depth and open interest have moved as expiry approaches.

- Rollover means closing or offsetting a position in the expiring contract and opening the equivalent exposure in a later contract month.

- Day traders usually roll charts and ladders when liquidity moves, not simply on the official expiry date.

- Cash-settled futures settle financially, while physically delivered futures can involve real delivery obligations if held too close to expiry.

- Futures spreads, including calendar spreads and butterflies, let traders trade the relationship between contract months rather than just the outright market direction.

- “Commission-free” CFDs or spread bets are not automatically cheaper than futures, because the true cost may be hidden in a wider spread, financing charge or rollover adjustment.

- Some futures contracts have price limits. A locked limit-up or limit-down market can stop a day trader exiting normally and may turn an intraday position into a full-margin overnight problem.